Saturday, December 15, 2012

Can Jumbo mortgage loan workouts reduce the sting of the next looming foreclosure wave?

Foreclosures increased in most large metropolitan areas over the first half of 2012 according to data released by foreclosure website RealtyTrac.com. Despite optimistic indicators such as the National Association of Home Builders/First American Improving Markets Index (IMI) for August showing that the housing market is improving [1], there remains a staggering 12 million mortgages with negative equity waiting to begin the foreclosure process. According to Brandon Moore, CEO of RealtyTrac, that amounts to $1.2 trillion.

Moore’s outlook for the economy is bleak at best as stated in an interview with Maria Bartiromo of CNBC, “I don’t know how the government should respond. I just know that I’m not hearing either presidential candidate talk about it and the current negative equity of properties that in the foreclosure process is $45 billion. You have 26 times that problem waiting to happen potentially.” [2] Fitch Ratings estimates that out of $381 billion in jumbo residential mortgage backed securities, almost 10% of the loans are seriously delinquent (more than 60 days past due).

There does appear to be some hope on the horizon. Homeowners with non-conforming jumbo mortgage loans (loans that failed to meet bank funding criteria set by FNMA due to loan limits) have recourse. A handful of specialty finance companies around the country are performing jumbo mortgage loan workouts on a case by case basis for homeowners who meet a set of requirements.

These finance companies offer to purchase the existing mortgage loan at a substantial discount for cash. They negotiate that amount with the lender for sometimes up to 50% of the mortgage balance. They restructure the homeowner's debt and provide long-term conventional financing at an amount not to exceed 80% of the market value of the home. This is done for a take-out at closing while not damaging the owner's credit and drastically lowering the principal balance and debt service. The homeowner pays little to nothing out of pocket. Homeowner requirements include very good credit scores above 700, a current mortgage, current taxes in paid status and no second mortgages or the second mortgage held by the same lender as the first mortgage. Homeowners need to take advantage of these offers now before the next wave of foreclosures.

Jumbo mortgage loan workouts are possible because of the National Mortgage Settlement reached in February 2012 between 49 state attorneys general and the nation’s five largest lenders, Ally/GMAC, Bank of America, Wells Fargo, Citi and JP Morgan Chase. The settlement provides relief to borrowers whose loans are serviced through these lenders including principal reductions. [3]

For more information, contact us at info@consumerdebtsolutions.net.

Author – Joan Villazon, C.F.O., Consumer Debt Solutions, Inc.

Website: www.consumerdebtsolutions.net

Facebook: www.facebook.com/debtfreedom

________________________________

[1] National Association of Home Builders. (2012) NAHB/First American Improving Markets Index (IMI) [Data File]. Retrieved from http://www.nahb.org/reference_list.aspx?sectionID=2223

[2] Video Transcript, July 25, 2012, CNBC.com, Bigger Mess Ahead for Foreclosure?

[3] National Mortgage Settlement. (2012). Federal Government & Attorneys General reach landmark settlement with major banks. Retrieved from http://nationalmortgagesettlement.com

Thursday, December 13, 2012

Free Credit Report

It's QUICK, EASY and SECURE. Request your free credit report>>

Annualcreditreport.com offers you the ability to pull your free credit report WITHOUT SCORES once per year from each of the credit reporting companies, Equifax, Experian and TransUnion. This process does not affect your credit in any way. It is important to see what's on your credit report at least once a year to verify that there are no inaccuracies reported that may be affecting your score.

When pulling your free credit report online, there are a series of security questions that you will be asked to ascertain your identity prior to allowing you access. If you cannot answer them, you are still able to send a letter directly to the credit reporting agency to request your report. Annualcreditreport.com gives you the information necessary to do so in the event this should occur.

When pulling your free credit report online, there are a series of security questions that you will be asked to ascertain your identity prior to allowing you access. If you cannot answer them, you are still able to send a letter directly to the credit reporting agency to request your report. Annualcreditreport.com gives you the information necessary to do so in the event this should occur.

There is an advantage to pulling all three credit reports at once. You have the opportunity to compare all three reports. You may find that not all credit reports will contain the same items. The only hitch is that you can only pull a free credit report once per year from each agency. If you have already done so and would like to pull your credit reports again, there are other options to obtain the "tri-bureau" reports.

Author: Joan Villazon

Consumer Debt Solutions, Inc., CFO

http://www.consumerdebtsolutions.net

Author: Joan Villazon

Consumer Debt Solutions, Inc., CFO

http://www.consumerdebtsolutions.net

Wednesday, December 12, 2012

Free Financial Tools

Auto Loan vs. Auto Lease Calculators

Compare purchasing vs. leasing a vehicle and see what fits into your budget.

Tuesday, December 11, 2012

Free Finance Classes Online

If you are searching for free finance classes online, you're in luck. There are several reputable, accredited universities offering courses that help you gain knowledge in estate planning, accounting, investing, taxation, economics, banking and personal financial planning. Most courses are offered without the pressures of exams and solely for your personal edification. These universities include Purdue, Yale, UC Irvine, Utah State, Rutgers, Carnegie Mellon and MIT to name a few. You may be wondering why these institutions would offer their course materials free of charge to anyone with internet connectivity. Many universities are subscribing to an open source philosophy where the internet is used for it's intended purpose which is the dissemination and sharing of ideas and information.

Consumer Debt Solutions, Inc.

Website: www.consumerdebtsolutions.net

Facebook: www.facebook.com/debtfreedom

I have listed the courses I found below. They are definitely not light reading and are truly college level quality but keep in mind that you are not being graded and you can take them at your own speed. Additionally, there are video lectures and courses that you can get through in an hour or less. Sit back and enjoy the opportunity to learn and take university courses free of charge. Free finance classes online may lead you to achieve financial peace of mind. Here's the list:

- Fundamentals of Personal Financial Planning: UC Irvine offers this class containing information on reaching financial goals like retirement and estate planning. Here's the outline for the course.

- Family Finance: Utah State University offers links to books, online resources and materials that help you to identify personal and family values and to set realistic financial goals.

- Investing for your Future: University of Kentucky Cooperative Extension Service offers a free course that six land-grant universities, the U.S. Department of Agriculture Cooperative State Research, Education, and Extension Service and the U.S. Securities and Exchange Commission put together.

- Economics: This page contains links to both undergraduate and graduate-level courses on economics.

- Investopedia University: Although not really an accredited university, this easy-to-navigate site offers dozens of free finance classes online from Forbes. Learn the basics of investing, trading, and retirement planning.

- Micro Economics: An OCW (OpenCourseWare) class on economics from Carnegie Mellon. Topics include as supply and demand, taxes, and monopolies.

- Investing for Your Future: This course from Rutgers Cooperative Extension takes students step-by-step through the investing process.

- Accounting Coach: This site offers detailed accounting lessons for the beginner.

- Money 101: CNN's Money 101 course helps you understand finance basics like investing, taxes, insurance and budgeting.

- Financial Markets ECON 252: This Yale University course offers the understanding of the theory of finance and its relation to the history of such institutions as banking, insurance, securities, futures, derivatives markets, and the future of these institutions over the next century.

- Planning for a Secure Retirement: Offered through Purdue Extension, includes 10 modules on retirement planning. The course content was developed by Sharon DeVaney, professor Emeritus. She specializes in the economics of aging.

Consumer Debt Solutions, Inc.

Website: www.consumerdebtsolutions.net

Facebook: www.facebook.com/debtfreedom

Friday, December 7, 2012

Life after debt – Set yourself up for success

How likely are you

to get back into debt after completing a debt consolidation plan?

Although debt

consolidation can help you repay your debt, it’s up to you to determine that

your life after debt remains debt free. Life Coaching can provide you with lasting

tools to help you stay on track and manage a spending plan to insure your

success.

Successful Life

After Debt Tip #1 – If you haven’t changed your spending habits, you could find

yourself in need of debt consolidation once again.

You are advised against taking on new credit card debt while you

are participating in a debt consolidation program. Be cautious about taking on

new debt after your program has ended. Many people swear off credit card debt

completely after the program but it’s unrealistic to expect that you will never

use credit or debt again in your lifetime. It’s a better idea to use credit

wisely than to think you will be able to stay away from it altogether.

Successful Life

After Debt Tip #2 – Always make your payments on time.

After building a three- to five-year positive payment history

through debt consolidation, you don’t want to jeopardize it with a single late

payment. Get in the habit of paying your credit card bills well before the due

dates to ensure your payment is processed in a timely manner. Timely

payments will help you maintain your interest rate, reduce the cost of carrying

credit and improve your credit.

Successful Life

After Debt Tip #3 – Start an emergency fund to avoid debt caused by financial

emergencies

That way, you have some savings to fall back on in case of a

financial emergency. Continue to maintain your emergency fund after you have

completed debt consolidation and avoid dipping into it unless it’s truly an

emergency.

The most important thing to remember when you are making new

credit card charges and applying for loans is that you should never take on

more than you can afford to repay. That means if you can only afford to pay

back a $10 credit card balance at the end of the month, then you should only

charge $10 on your credit card. Before you swipe your credit card, assess

whether you will have enough money to pay back the balance.

Successful Life

After Debt Tip #4 – Focus on managing your money wisely

The smarter you are with your money, the less likely it is that

you will resort to credit cards and debt to maintain your life. Good money

management starts with a spending plan. Having a spending plan helps guide your

spending and allows you to recognize any gaps between your income and your expenses.

Seeing your expenses on paper makes it easier to evaluate your expenses and

reduce them if necessary.

Successful Life

After Debt Tip #5 – Staying out of debt will take much self-discipline.

Don’t be afraid to close your credit card

accounts if you are tempted to use them to charge more than you can afford. Although the debt consolidation company

would love to have you back as a customer, it is in your best interest to stay

out of debt.

Tuesday, December 4, 2012

Fiscal Policy and the Fiscal Cliff

In

the United States, fiscal policy is established through taxation to generate

revenues and the increase or decrease of government spending. The President and Congress are responsible

for determining the fiscal policy which ultimately affects the American

economy. Three main elements of the

economy are directly affected. These include aggregate demand, resource

allocation and distribution of income.

An

expansionary policy attempts to keep government spending above tax revenues and

is usually implemented during recessions to stimulate aggregate demand, as has

been the case over the past 12 years and in accordance with the economic theory

put forward by John Maynard Keynes. A

contractionary policy keeps government spending below tax revenues to pay down

the national debt and is implemented to stabilize prices during inflationary

economies, if Keynesian theory is accurate.

There

are opposing views by classical and neoclassical economists that argue the “crowding

out” effect of government spending. This viewpoint posits that when government

spending is in excess of revenues, the government must borrow funds from other

countries, issue government bonds and cause interest rates to rise. This results

in higher demand in the financial markets, lower demand for goods and services

and the government then appears to crowd out private sector spending.

These

two opposing economic theories are important to keep in mind as the White

House, Congress and both political parties attempt to arrive at a compromise to

begin paying off the national debt. The

two theories shed light on why it is so difficult for democrats and republicans

to strike a deal in the face of the impending fiscal cliff. Republicans appear to be favoring a

contractionary scenario where government spending is substantially reduced and

taxes remain low while democrats are favoring an expansionary scenario in which

government spending is increased and taxes are also increased. These

differences of opinion are difficult to overcome because they involve philosophical

beliefs and the correctness of each is not readily visible.

Article by: Joan Villazon, CFO

Consumer Debt Solutions, Inc.

Monday, December 3, 2012

What is Monetary Policy?

This is a very brief overview of how Monetary Policy is carried out in the U.S. Monetary Policy can affect the decisions of consumers to buy or sell houses, cars, take out loans, start businesses, apply for credit cards, open bank accounts and so on. The Federal Reserve is responsible for setting monetary policy in the United States. Ideally, the Federal Reserve aims to control inflation, employment and output through a small arsenal of tools at its disposal. The Federal Reserve achieves its goals by manipulating demand - the tendency of consumers and businesses to spend on goods or services.

The tools used by the Federal Reserve are as follows:

Bank Reserves –The amount banks are required to keep in order to meet outflows or withdrawals. The Fed can raise or lower the requirement depending upon whether it wants to stimulate inter-bank lending.

Fed Funds Rate – The interest rate at which banks lend money to each other to meet the bank reserves requirement. A higher rate would be set if the supply of reserves available to lend is less than the demand for those reserves. The converse is also true. If the supply of reserves is greater than the demand, the rate is lowered.

Open Market Operations – The Federal Reserve Bank of New York will either buy or sell government bonds on the open market. When the fed purchases government bonds from a bank, the resulting transaction increases the reserve supply of that bank. The bank is then able to lend the surplus reserves to other banks and the fed funds rate drops.

Discount Rate – The interest rate at which a bank can go directly to the Federal Reserve to borrow funds. The Fed typically keeps this rate higher than the Fed funds rate in order to make sure that banks borrow from each other.

It is difficult for the Federal Reserve to utilize these tools effectively because of the operational lag between exercising new policy and seeing its effects. The Fed does not know exactly when a change in policy will cause a desired effect. The Fed also cannot afford to wait to see the effects of a policy change and must anticipate what changes it needs to make before the economy has an actual shift. Economic indicators are used to gauge the direction of the economy and take pre-emptive measures.

Article by: Joan Villazon, CFO

Consumer Debt Solutions, Inc.

http://www.consumerdebtsolutions.net

The tools used by the Federal Reserve are as follows:

Bank Reserves –The amount banks are required to keep in order to meet outflows or withdrawals. The Fed can raise or lower the requirement depending upon whether it wants to stimulate inter-bank lending.

Fed Funds Rate – The interest rate at which banks lend money to each other to meet the bank reserves requirement. A higher rate would be set if the supply of reserves available to lend is less than the demand for those reserves. The converse is also true. If the supply of reserves is greater than the demand, the rate is lowered.

Open Market Operations – The Federal Reserve Bank of New York will either buy or sell government bonds on the open market. When the fed purchases government bonds from a bank, the resulting transaction increases the reserve supply of that bank. The bank is then able to lend the surplus reserves to other banks and the fed funds rate drops.

Discount Rate – The interest rate at which a bank can go directly to the Federal Reserve to borrow funds. The Fed typically keeps this rate higher than the Fed funds rate in order to make sure that banks borrow from each other.

It is difficult for the Federal Reserve to utilize these tools effectively because of the operational lag between exercising new policy and seeing its effects. The Fed does not know exactly when a change in policy will cause a desired effect. The Fed also cannot afford to wait to see the effects of a policy change and must anticipate what changes it needs to make before the economy has an actual shift. Economic indicators are used to gauge the direction of the economy and take pre-emptive measures.

Article by: Joan Villazon, CFO

Consumer Debt Solutions, Inc.

http://www.consumerdebtsolutions.net

Friday, November 30, 2012

Hiring a Tax Preparer

The IRS began the process of regulating all paid tax return preparers in 2011. A PTIN or Preparer Tax Identification Number is now required by all tax preparers. The government required that all licensed professionals renew their PTIN as well. This includes CPA's, Attorneys and Enrolled Agents (EA's).

Why is this important? Well, up until 2011, anyone could prepare a tax return for pay without any suitability check and without being licensed or regulated. Only those professionals with a CPA, EA or a lawyer had to adhere to strict regulations. This is changing by the end of 2013 when all legitimate tax preparers will be required to have an RTRP designation. RTRP stands for Registered Tax Return Preparer and the designation is granted via a competency exam that covers the 1040 series of forms and the Circular 230 covering professional ethics. All legitimate tax preparers will also be required to have the PTIN until the IRS stops issuing them.

Because the new regulations don't take effect until 2014, there will still be those unlicensed and possibly unethical individuals who have not passed any competency exam preparing taxes without knowing or caring about your best interest. The use of a PTIN does not guarantee that the tax preparer you are employing is qualified or licensed. Please use diligence in hiring a tax preparer. Look for the proper designations such as RTRP, EA, CPA or tax attorney. At the very minimum, your tax professional should posses an RTRP designation. This ensures that your tax return preparer is accountable to the IRS when he/she signs your tax return.

Article by: Joan Villazon, CFO

Consumer Debt Solutions, Inc.

http://www.consumerdebtsolutions.net

Thursday, November 29, 2012

What is the AMT?

AMT refers to the flat Alternative Minimum Tax devised by the government in 1969 as a tool to keep the wealthiest of taxpayers from avoiding their fair share of tax payments with large deductions and loopholes. The AMT runs parallel to the regular income tax and makes the taxpayer pay the higher of the two taxes. The problem is that the Alternative Minimum Tax was not adjusted for inflation and has begun to affect middle class income earners. Taxpayers falling under the AMT will pay an average $2000 more in taxes than they would without the AMT.

The taxpayers most at risk for paying the AMT tax rate are usually married with two or more children and own homes located in states with high income taxes such as California, Michigan and New York. The reason these particular taxpayers are affected is because the government will not allow all of the tax deductions to lower their taxable income. The deductions are viewed as excessive. The following items normally trigger the AMT:

Note that the first two items are common to many taxpayers owning a home. The remaining items refer to investments and self employment income. There is no real income level in which a taxpayer falls under the AMT. Rather, the qualification for AMT is dictated by the percentage of income that deductions amount to. As it currently stands, the AMT tax rate is 26% on the first $175,000 of AMT taxable income and 28% on the remainder of AMT taxable income

There is an exemption to the AMT if taxpayers qualify for the higher tax. Under the tax relief act of 2010 the exemption amounts were increased substantially. If the fiscal cliff is allowed to occur without congressional intervention, the exemption is scheduled to go back to $33,750 for single and head of household taxpayers, $45,000 for married filing jointly and/or qualifying widows or widowers and $22,500 for married people filing separately. What this means is that if a taxpayer qualifies for the AMT, the exemption amounts referred to above are not taxed at the AMT rate. Lower exemption amounts will result in a greater number of taxpayers having to pay the AMT rate.

Article by: Joan Villazon, CFO

Consumer Debt Solutions, Inc.

http://www.consumerdebtsolutions.net

The taxpayers most at risk for paying the AMT tax rate are usually married with two or more children and own homes located in states with high income taxes such as California, Michigan and New York. The reason these particular taxpayers are affected is because the government will not allow all of the tax deductions to lower their taxable income. The deductions are viewed as excessive. The following items normally trigger the AMT:

- Itemized deductions for state and local taxes, medical expenses, and miscellaneous expenses

- Mortgage interest on home equity debt

- Accelerated depreciation

- Exercising incentive stock options

- Tax-exempt interest from private activity bonds

- Passive income or losses

- Net operating loss deduction

- Foreign tax credits

- Investment expenses

Note that the first two items are common to many taxpayers owning a home. The remaining items refer to investments and self employment income. There is no real income level in which a taxpayer falls under the AMT. Rather, the qualification for AMT is dictated by the percentage of income that deductions amount to. As it currently stands, the AMT tax rate is 26% on the first $175,000 of AMT taxable income and 28% on the remainder of AMT taxable income

There is an exemption to the AMT if taxpayers qualify for the higher tax. Under the tax relief act of 2010 the exemption amounts were increased substantially. If the fiscal cliff is allowed to occur without congressional intervention, the exemption is scheduled to go back to $33,750 for single and head of household taxpayers, $45,000 for married filing jointly and/or qualifying widows or widowers and $22,500 for married people filing separately. What this means is that if a taxpayer qualifies for the AMT, the exemption amounts referred to above are not taxed at the AMT rate. Lower exemption amounts will result in a greater number of taxpayers having to pay the AMT rate.

Article by: Joan Villazon, CFO

Consumer Debt Solutions, Inc.

http://www.consumerdebtsolutions.net

Monday, November 26, 2012

Should Social Security endure another year of cuts?

The Congressional Budget Office (CBO) released its’ report on the state of the Social Security program on October 2, 2012. In the report, the CBO shows that the Social Security program had more expenditures than tax revenue in 2011, the result of two years of a payroll tax cut included in a negotiated deal on tax policy between President Obama and congressional Republicans.

The shortfall, as stated by trustees of the Social Security program, does not take into account the interest earned by Social Security assets (special issue U.S. Treasury securities). When including accrued interest, income exceeded expenditures by $69 billion. The main concern is the ever increasing number of retiring baby boomers who will burden the system to the point of exceeding tax revenues by 20% in 2030.

The shortfall, as stated by trustees of the Social Security program, does not take into account the interest earned by Social Security assets (special issue U.S. Treasury securities). When including accrued interest, income exceeded expenditures by $69 billion. The main concern is the ever increasing number of retiring baby boomers who will burden the system to the point of exceeding tax revenues by 20% in 2030.

Given the findings, the pressure is on to extend the payroll tax cut for an additional year. However, how wise was it to negotiate the cut in the first place? Presumably, the original intention of the tax cut was to boost consumer spending in an effort to stimulate a sluggish economy and increase GDP. If the tax cuts are extended, GDP is forecast to grow by 1%. If the tax cuts are not extended and the fiscal cliff is allowed to occur without congressional action, GDP is forecast to increase by a dismal .5%, theoretically throwing the country into recession. Should the Social Security program tolerate another year of cuts? You do the math.

Article by:

Joan Villazon, C.F.O

Consumer Debt Solutions, Inc.

www.consumerdebtsolutions.net

Thursday, November 15, 2012

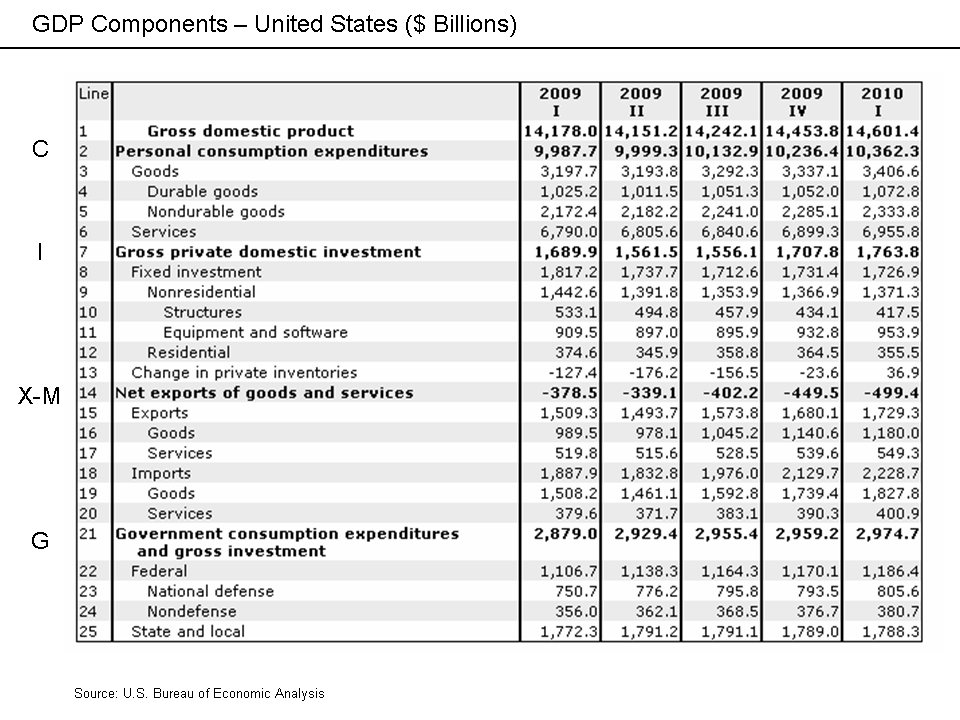

What is the GDP?

GDP refers to Gross Domestic Product and it is one of the tools that measures the economic health of the nation. There are two approaches to calculating GDP, the income approach and the more common expenditure approach.

The income approach involves adding up:

1. total wages, salaries, and supplementary income plus

2. corporate profits

3. interest and miscellaneous investment income

4. farmers’ income

5. income from non-farm unincorporated businesses

6. indirect taxes minus subsidies and

7. depreciation.

The expenditure approach involves adding up:

1. consumption - private spending on durable and non-durable goods and services

2. investment - business spending on equipment and household spending on new housing

3. government spending - on final goods, public servant salaries and military spending and

4. net exports - total exports minus total imports.

GDP can also be thought in terms of production. It is the total value of everything produced by all people and companies within the country. The Bureau of Economic Analysis (BEA) reports on Real GDP (GDP adjusted for inflation). Last year, GDP was $15.3 trillion.

Why is GDP important? Economic growth or contraction is measured by the change in GDP from quarter to quarter. This makes GDP important to everyone since it impacts employment and stock prices. Negative growth in GDP is one of the leading indicators for whether the economy is in a recession. The Federal Reserve makes monetary policy decisions surrounding GDP. Following GDP statistics can help prepare consumers for future layoffs if the growth rate is negative or for higher interest rates if the growth rate is increasing.

Joan Villazon

CFO

Consumer

Debt Solutions, Inc.Become a Fan: www.facebook.com/debtfreedom

Subscribe to:

Posts (Atom)